Employers need to understand Capital Accumulation Plan (CAP) guidelines

Did you know that the CAP guidelines were enacted by the Joint Forum of Financial Market Regulators in 2004? I’m amazed at the number of businesses I meet that are not really sure about what this means to them.

If you are an employer and you have a Defined Contribution Pension Plan, group RRSP plan, group RESP plan or a deferred profit sharing plan, then you have a set of responsibilities under the Capital Accumulation Plan Guidelines.

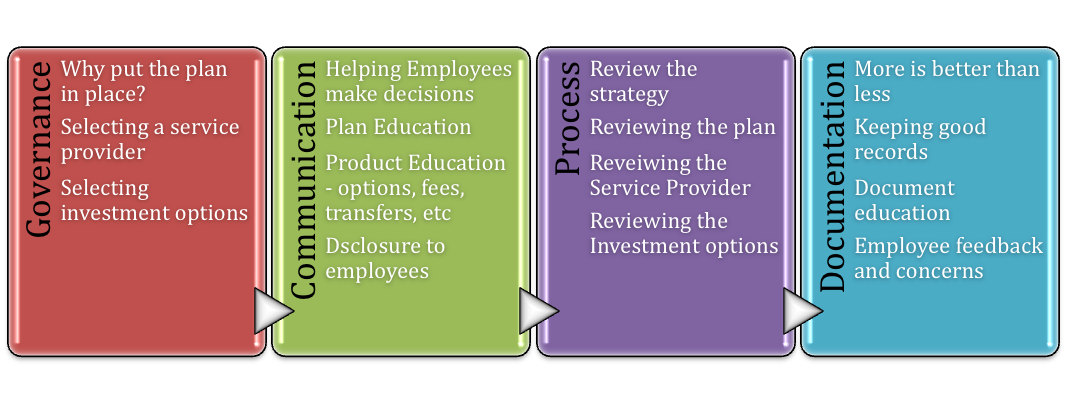

According to the 18-page document put together by the regulators, employers have a new set of responsibilities. Here is a summary of the requirements broken down into four key themes: Governance, Communication, Process and Documentation.

{kind=link}

Governance – A strategy document.

One of the themes of the CAP guidelines is the theme of governance. Generally speaking the plan sponsor or employer is required to outline the criteria for establishing the plan, the service provider and the investments being offered through the plan. The best thing to do is put these criteria in writing as a strategy or governance document. Here are some of the things that document might include:

What is the purpose of the plan? In other words, why is the plan implemented? There could be many reasons which might include:

- To help employees with retirement savings

- To help employees become more fiscally responsible

- To attract and retain good employees

- To reward employees

If there is change to the plan or the purpose of the plan, it should be documented as well. This document should be reviewed periodically or when significant changes occur.

In some cases, Group RRSP or Pension plans have been around for so long and has survived numerous management teams. This is a good opportunity for review.

Are you going to use a service provider? If the intent is to use a service provider (broker or consultant), the document should also outline some criteria for choosing a broker or consultant and then monitor the service provided against those criteria on a regular basis. Some of the criteria for selection might include: professional training, experience, specialization, fees, quality of services, etc.

Part of choosing a service provider is knowing what roles and responsibilities they are going to take on. The Strategy Document should outline the roles and responsibilities of the Plan Sponsor (employer), Service provider (broker and/or financial institution, and the members (employee).

Communication and education

Another big component of the CAP guidelines is the requirement for communication and education. This can be a big responsibility for the employer. Here are some things to consider:

- Although employees or CAP members are responsible for making investment decisions within the plan, the employer is required to provide adequate information on the plan and the investment options. The CAP sponsor should also provide the employees/members with the tools necessary to make investment decisions within the plan. More often than not the service provider provides online tools, documents and questionnaires to help employees make appropriate decisions.

- According to the most recent research by Benefits Canada, a high proportion (86%) of employers feel they are providing education and information to employees for the purpose of making sound choices in the plan. Most employers and service providers provide the minimum level of information, education and tools. In other words most of the education that occurs is plan and product education where employees are given information on the plan, how it works and the investments inside the plan. It is important for the employer to explain the investment options, transfer options, fees, expenses and penalties around the plan.

- Some employers are going beyond these minimum education standards by providing financial education, which really broadens the scope of information, and education. Instead of helping employees with one small aspect of their personal finances, some employers are implementing financial education programs designed to help employees with all facets of their financial lives and not just the impact of the group plan.

- We encourage all employers to consider a financial education program to complement their existing educational requirements. The cost is minimal and the results can be astounding.

Process – Plan maintenance

The last major theme around the CAP guidelines is the requirement to maintain the plan. In the guidelines, there is quite a bit of information about setting periodic reviews of many aspects of the plan including a review of service providers, review of the plan, review of the investment options. This is where a broker or consultant can really help because they can take a lot of the review requirements off the plate of the employer.

Documentation

The bottom line is documentation is so important in the world of regulation. The whole point of regulation is to protect interested parties. Employers need to protect themselves through documentation as does the service provider and event the employee.

As part of a good governance structure, anything important must be documented. This includes the relationship with service providers—a contract with each of them is essential. The investment selection process and periodic reviews also need to be documented.

The Guidelines recommend a document retention policy be prepared and maintained. While several plan sponsors have mentioned that there is a significant amount of work to be done here, a well-documented process is an excellent risk management tool. And make sure privacy legislation is built in to your document retention policy.

Keep one file or binder for compliance. One of the things we do to help our clients with the CAP guidelines is to maintain what we call a compliance binder. In case of an audit, this binder will provide documentation that will ensure that the guidelines are met or exceeded. Although it is the plan sponsor or employers responsibility, we make every effort to make the task of being compliant as easy as possible. The binder should contain all relevant documents described above:

- The strategy or governance document

- Any communication that has occurred within the plan

- Employee feedback

- Employee complaints

Who’s responsible?

While service providers such as fund managers, third-party administrators and record-keepers have been hard at work to ensure compliance from their end, it remains the task of CAP sponsors to review and ensure that the intent of the Guidelines is met by their governance agendas.

The CAP Guidelines reflect the expectations of regulators regarding the operation of a capital accumulation plan, regardless of the regulatory regime applicable to the plan. They are intended to support the continuous improvement and development of industry practices.

The Guidelines are based on what were already best practices in the industry, so compliance shouldn’t be a big stretch for most organizations.

Developing a sound process with the CAP Guidelines in mind has tremendous benefits:

- clarifying the accountabilities and rights of CAP members, sponsors and service providers;

- protecting against legal risks;

- providing a framework for efficient plan administration;

- and ensuring that CAP members are provided with the information and assistance they need to make investment decisions in a CAP.

Whether this sound new to you or sounds like you have it all covered, it’s never a bad thing to review your group retirement plan or get some help from a group benefits expert.

Comments

If you read the first paragraph of the guideline, you will find that if you don’t provide employees with individual investment choice, the guideline doesn’t apply.

Investment choice increases legal risk and adversely affects performance and increased cost.